Of Time Deposits, SDAs and Credit Rating - What's in it for the Savers and Non-Savers?

"Han, upgraded to investment grade na ang Philippines sa Fitch." ("Han, Philippines has been upgraded to investment grade by Fitch.") - This was a text message I got from my client last March 27, 2013 at around 2:48pm.

As a non-day trader, non-economist, and somebody who graduated from an engineering course but saw a career in the financial consultancy field, I knew right there and then that it was good news.

However, the non-economist side of me kicked in. What's in it for me as a regular investor? As a non-stock trader? How do I translate this good news to my existing clients and prospects in a way that can be understood by somebody not in the investment field, i.e. the savers and non-savers?

This article will be an attempt on that. Wish me luck! Now, if I'm able to accomplish my objective, will you be kind enough to share the information to your friends? Thanks!

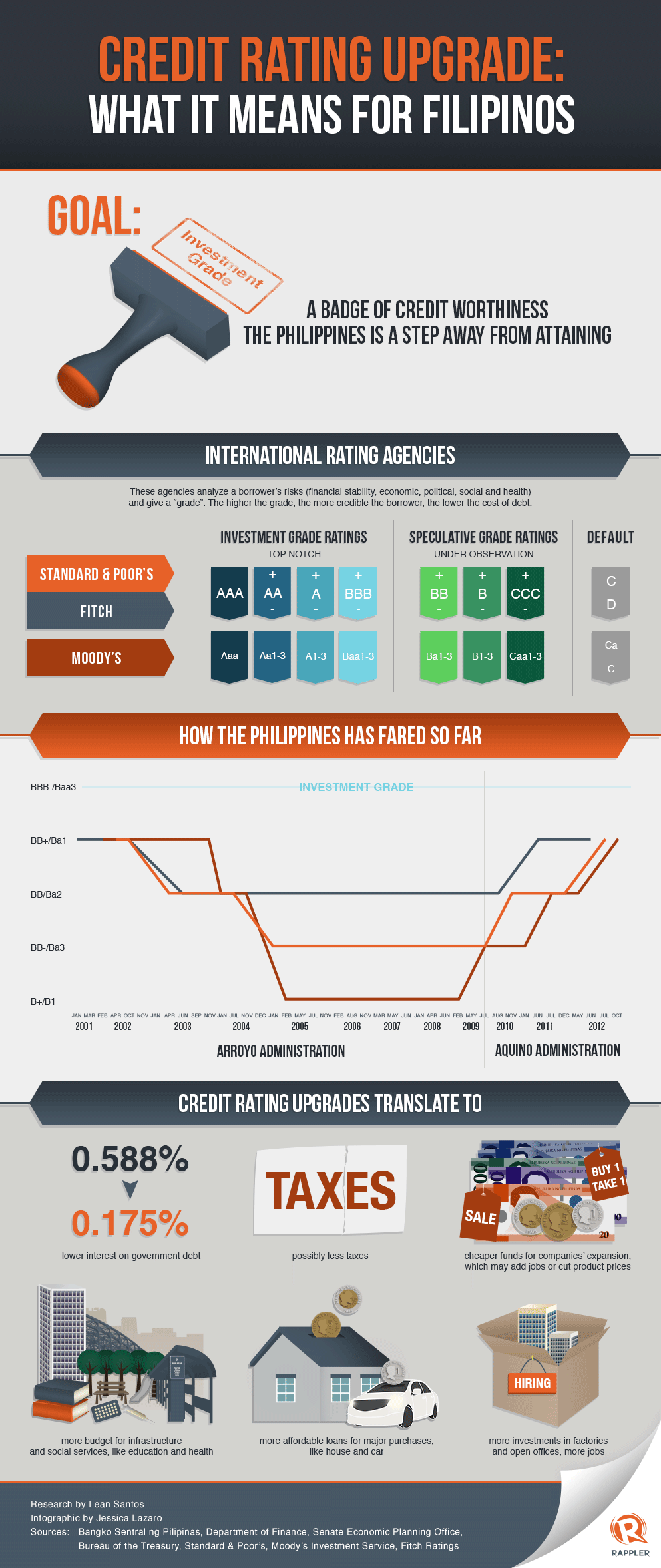

Anyway, the moment I got that text message from my day-trader client, I had to check my regular resource sites for that same news. And good thing, I saw an infographic that helped explain about the credit rating upgrade from one of my sources! :) Thank you Rappler for this nice infographic.

Now, I would like to focus more on the effects of a credit rating upgrade...

Lower interest on gov't debt.

If you're somebody who plans to buy more bonds, placing money in TDs (time deposits) or SDAs (special deposit accounts) then this will be bad news for you... Well, good news for our gov't but bad news for the one lending there money to. Why? SDA and TD rates are close enough to T-bills and RoP Bond rates. They're pegged at that rate just enough to beat the inflation. But sometimes, inflation outpaces them. Here's a graph to show you how it looks like.

However, for those staying away from the stock market because its "risky", here's a picture I'd like to share to you on the risk that you're staying away from.

Money Value Calculator Exercise:

Now, if you've been placing money in the bank or plan to park money in the bank with the intent to grow it, I encourage you to do this exercise with me.

Since 2001, the average inflation is at 4.28%. So for inflation rate purposes, we'll just use 4% (or 0.04). Now, for this exercise I decided to benchmark on the rates of the bank I'm using, BPI, Bank of the Philippine Islands*. As per their site, the highest TD rate is at 1.5% (or 0.015) good for 364 days. But you need to put in at least 5 million pesos.

Using the calculator below, how much do you think you've grown your money? Has it really grown?

Note: In order for the calculator to work as expected, use the decimal form of interests.

(For the sake of those who are not into numbers:

i.e. 0.1%/100 = 0.001

1%/100 = 0.01

10%/100 = 0.1)

Well, your passbook might show a gross growth of P75,000 (called as the nominal value) after a year of parking P5,000,000 in TD, but in reality, after considering inflation, you've lost P125,000 worth of goods since you were not able to grow your P5,000,000 in the same rate as inflation. The real value of your P5,000,000 after 1 year should be at P5,200,000 in order for you to purchase the same amount of goods prior to parking your money.

How does this calculator work? It will help you to compute by how much you've grown the purchasing power of your investment. If the result shows a positive result, then you've increased the amount of goods purchased by that amount. However, if the result is a negative number, then you've lost that amount of goods to inflation. Ergo, you lost money to inflation.

Now, you try it! Here's a site where you can check the different rates of different banks in the Philippines, http://philippines.deposits.org/. And tell me if you've grown your money or you lost money to inflation.

Whatever the result is, whether it's a positive one or a negative one, feel free to comment and I'll give a little token of appreciation. :)