"Han, upgraded to investment grade na ang Philippines sa Fitch." ("Han, Philippines has been upgraded to investment grade by Fitch.") - This was a text message I got from my client last March 27, 2013 at around 2:48pm.

As a non-day trader, non-economist, and somebody who graduated from an engineering course but saw a career in the financial consultancy field, I knew right there and then that it was good news.

However, the non-economist side of me kicked in. What's in it for me as a regular investor? As a non-stock trader? How do I translate this good news to my existing clients and prospects in a way that can be understood by somebody not in the investment field, i.e. the savers and non-savers?

This article will be an attempt on that. Wish me luck! Now, if I'm able to accomplish my objective, will you be kind enough to share the information to your friends? Thanks!

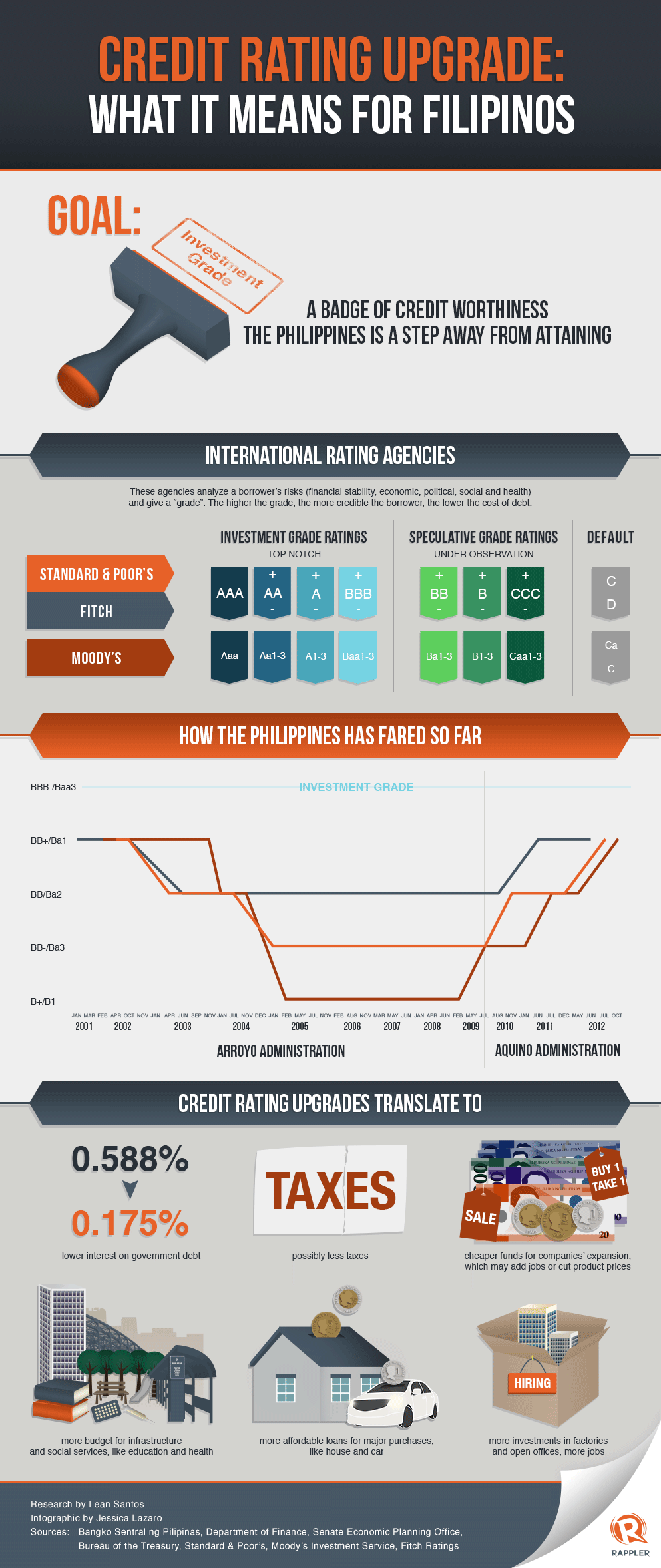

Anyway, the moment I got that text message from my day-trader client, I had to check my regular resource sites for that same news. And good thing, I saw an infographic that helped explain about the credit rating upgrade from one of my sources! :) Thank you Rappler for this nice infographic.

Now, I would like to focus more on the effects of a credit rating upgrade...

Lower interest on gov't debt.

As a non-day trader, non-economist, and somebody who graduated from an engineering course but saw a career in the financial consultancy field, I knew right there and then that it was good news.

However, the non-economist side of me kicked in. What's in it for me as a regular investor? As a non-stock trader? How do I translate this good news to my existing clients and prospects in a way that can be understood by somebody not in the investment field, i.e. the savers and non-savers?

This article will be an attempt on that. Wish me luck! Now, if I'm able to accomplish my objective, will you be kind enough to share the information to your friends? Thanks!

Anyway, the moment I got that text message from my day-trader client, I had to check my regular resource sites for that same news. And good thing, I saw an infographic that helped explain about the credit rating upgrade from one of my sources! :) Thank you Rappler for this nice infographic.

Now, I would like to focus more on the effects of a credit rating upgrade...

Lower interest on gov't debt.

So, if our gov't would have to borrow money, either from it's people or some foreign entity, the rate that they'll be borrowing will be lower to what we're experiencing right now. Now, what are these gov't debts? From my understanding (If an economist reads this, please correct me if I'm wrong in my understanding. Again, this is based on my non-economist side.) sample instruments of gov't debts are T-bills and RoP Bonds.

If you're somebody who plans to buy more bonds, placing money in TDs (time deposits) or SDAs (special deposit accounts) then this will be bad news for you... Well, good news for our gov't but bad news for the one lending there money to. Why? SDA and TD rates are close enough to T-bills and RoP Bond rates. They're pegged at that rate just enough to beat the inflation. But sometimes, inflation outpaces them. Here's a graph to show you how it looks like.

Just now, I saw an article stating that the T-bill rates has dropped to its all time low.

More affordable loans.

Cheaper funds for company expansions; More investments in factories and open offices, more jobs.

Money Value Calculator Exercise:

Now, if you've been placing money in the bank or plan to park money in the bank with the intent to grow it, I encourage you to do this exercise with me.

Since 2001, the average inflation is at 4.28%. So for inflation rate purposes, we'll just use 4% (or 0.04). Now, for this exercise I decided to benchmark on the rates of the bank I'm using, BPI, Bank of the Philippine Islands*. As per their site, the highest TD rate is at 1.5% (or 0.015) good for 364 days. But you need to put in at least 5 million pesos.

Using the calculator below, how much do you think you've grown your money? Has it really grown?

Note: In order for the calculator to work as expected, use the decimal form of interests.

(For the sake of those who are not into numbers:

i.e. 0.1%/100 = 0.001

1%/100 = 0.01

10%/100 = 0.1)

Well, your passbook might show a gross growth of P75,000 (called as the nominal value) after a year of parking P5,000,000 in TD, but in reality, after considering inflation, you've lost P125,000 worth of goods since you were not able to grow your P5,000,000 in the same rate as inflation. The real value of your P5,000,000 after 1 year should be at P5,200,000 in order for you to purchase the same amount of goods prior to parking your money.

How does this calculator work? It will help you to compute by how much you've grown the purchasing power of your investment. If the result shows a positive result, then you've increased the amount of goods purchased by that amount. However, if the result is a negative number, then you've lost that amount of goods to inflation. Ergo, you lost money to inflation.

Now, you try it! Here's a site where you can check the different rates of different banks in the Philippines, http://philippines.deposits.org/. And tell me if you've grown your money or you lost money to inflation.

Whatever the result is, whether it's a positive one or a negative one, feel free to comment and I'll give a little token of appreciation. :)

If you're somebody who plans to buy more bonds, placing money in TDs (time deposits) or SDAs (special deposit accounts) then this will be bad news for you... Well, good news for our gov't but bad news for the one lending there money to. Why? SDA and TD rates are close enough to T-bills and RoP Bond rates. They're pegged at that rate just enough to beat the inflation. But sometimes, inflation outpaces them. Here's a graph to show you how it looks like.

Due to the rising confidence of depositors in banks, the bank has now a huge chunk of deposits that needs to circulate. As of 2012, there are over P4.5T in the Philippine banking system. And the only way for this to circulate is to lend it to the public. And to entice people to borrow, they lower down the borrowing rate.

More affordable loans means more opportunity to create new businesses (either small, medium or large) or even expand. Now for those trading / investing in the stock market that's good news for you as well! Why? Expansions or new business by these companies will grow the value of your shares! :)

However, for those staying away from the stock market because its "risky", here's a picture I'd like to share to you on the risk that you're staying away from.

However, for those staying away from the stock market because its "risky", here's a picture I'd like to share to you on the risk that you're staying away from.

Some companies composing the PSEi.

Looking at this picture, do you really think these companies will be defaulting ALL at the same time in the near future? Granting you don't have any idea on which company is good enough to invest in or stay away from, then a professionally managed fund is a better option for you - i.e mutual funds, UITF (unit-investment trust fund) or variable unit linked (VUL) products.

This is a graph showing you the yearly performances of different investment vehicles - from savings deposit accounts, time deposits, SDAs (special deposit accounts), mutual funds, t-bills and some of the benchmarks such as core inflation rate and PSEi performance.

If you had invested P1 in each of these vehicles since 2000, how much do you think the value of your P1 is today?

In order to maintain the purchasing power of your P1 back in 2000, you should be able to grow it at the same rate as inflation. The graph shows that in order to buy the same amount of goods for your P1 back in 2000, your P1 should now be at P1.72. Unfortunately, bank products and even the 364-day T-bills where not able to grow the P1 at that level since 2001. If you had placed your money in TDs, SDAs, Tbills, worse, in savings account since 2000, you have lost more value to your money.

But! The "risky" ones, were able to double, quadruple and more for your P1. That is net of inflation already.

Risk is relative. Crossing the street, either on foot or riding a vehicle, involves risk. You could slip, you could get hit by a car or be bumped by another person. But we still do it on a daily basis. Why? To get to our destination. Same thing goes for our savings. Savers would like to grow their money. However, they forgot to consider inflation - that thing that sucks the value out of your money - keeping you from reaching your destination.

Money Value Calculator Exercise:

Now, if you've been placing money in the bank or plan to park money in the bank with the intent to grow it, I encourage you to do this exercise with me.

Since 2001, the average inflation is at 4.28%. So for inflation rate purposes, we'll just use 4% (or 0.04). Now, for this exercise I decided to benchmark on the rates of the bank I'm using, BPI, Bank of the Philippine Islands*. As per their site, the highest TD rate is at 1.5% (or 0.015) good for 364 days. But you need to put in at least 5 million pesos.

Using the calculator below, how much do you think you've grown your money? Has it really grown?

Note: In order for the calculator to work as expected, use the decimal form of interests.

(For the sake of those who are not into numbers:

i.e. 0.1%/100 = 0.001

1%/100 = 0.01

10%/100 = 0.1)

Well, your passbook might show a gross growth of P75,000 (called as the nominal value) after a year of parking P5,000,000 in TD, but in reality, after considering inflation, you've lost P125,000 worth of goods since you were not able to grow your P5,000,000 in the same rate as inflation. The real value of your P5,000,000 after 1 year should be at P5,200,000 in order for you to purchase the same amount of goods prior to parking your money.

How does this calculator work? It will help you to compute by how much you've grown the purchasing power of your investment. If the result shows a positive result, then you've increased the amount of goods purchased by that amount. However, if the result is a negative number, then you've lost that amount of goods to inflation. Ergo, you lost money to inflation.

Now, you try it! Here's a site where you can check the different rates of different banks in the Philippines, http://philippines.deposits.org/. And tell me if you've grown your money or you lost money to inflation.

Whatever the result is, whether it's a positive one or a negative one, feel free to comment and I'll give a little token of appreciation. :)