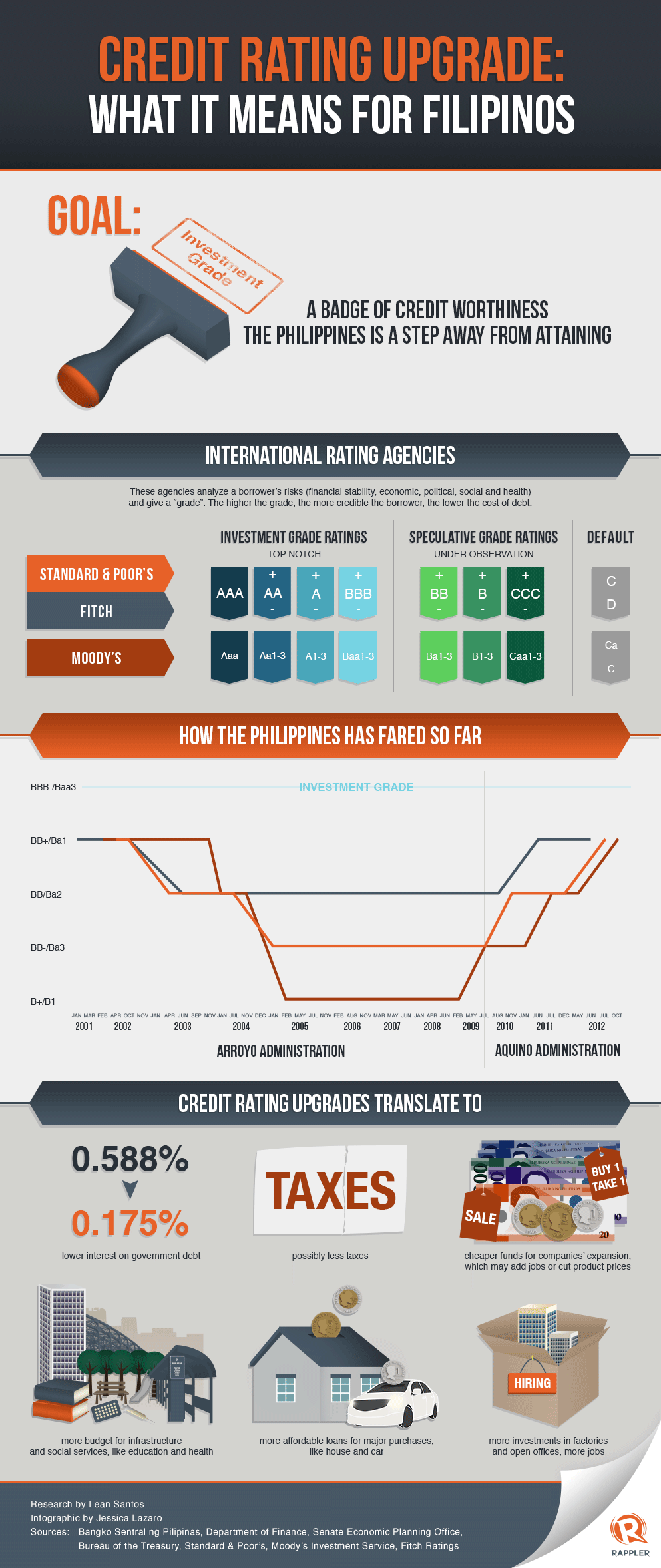

It's been almost a month since Yolanda struck our country. It's been one surreal experience for those who survived and a great loss to everyone.

I myself was too busy coordinating on the retrieval of some relatives who lived in Tacloban when I was asked this question:

"What will happen to those victims who have previous loans in the bank, credit cards to pay, jewelries or valuable items kept safe inside the bank? How will they be able to fulfill their obligation to pay when they have lost (******) everything?"

Based on my professional point of view and understanding, my response was:

"An obligation is an obligation. A debt is a debt. Doesn't necessarily mean that the calamity has washed away everything, it doesn't necessarily wash away their debts and obligations. However, these institutions (the creditors) do give extensions on the payment."

That was my quick and short response. But after that, I decided to ask for further details on the affected institutions and ways to address this certain kind of risk.

Payment of debts - A banker friend of mine who's task is into generating loans, she confirmed my quick and short response. She also mentioned to me that in their bank, they would usually give a 90 day extension for the debtors to pay off their dues. Penalties are also waived off.

So, if you are affected by Yolanda and your concern is on the payment of your outstanding debts, just approach your creditor and explain to them the situation. I'm pretty sure they will be more lenient with their debtors.

How can they rebuild their lives?

So, yeah! How can one protect one's self from this kind of risk? Time and again, I have heard of studies stating how Japan gets to rebuild itself even it being one country that get's hit by a lot of calamities. The answer to this is INSURANCE.

Japan is the second biggest insurance market in the world after the U.S. and generates nearly 20% of global premiums. In our industry training, it has been shared to us how Japan picks itself up after someone passes away. A Japanese have an average of 7 insurance policies. So, when a Japanese dies, his beneficiaries receives funds that can help them rebuild their lives.

We can't keep on relying on outside help to rebuild our lives. There are ways to minimize our exposure to the damages of these kind of calamities. Unfortunately, majority of the population have no idea of what's available out there.

As they say, "Nobody plans to fail, they just fail to plan."

So, let's all learn the lesson here. There are ways to manage these risks, it's a matter of asking the right people how. We can help you protect your biggest investment. You may reach us via admin@honeycombfc.com or reach us on Facebook.

I myself was too busy coordinating on the retrieval of some relatives who lived in Tacloban when I was asked this question:

"What will happen to those victims who have previous loans in the bank, credit cards to pay, jewelries or valuable items kept safe inside the bank? How will they be able to fulfill their obligation to pay when they have lost (******) everything?"

|

| I don't own credit to this image. |

Based on my professional point of view and understanding, my response was:

"An obligation is an obligation. A debt is a debt. Doesn't necessarily mean that the calamity has washed away everything, it doesn't necessarily wash away their debts and obligations. However, these institutions (the creditors) do give extensions on the payment."

That was my quick and short response. But after that, I decided to ask for further details on the affected institutions and ways to address this certain kind of risk.

Payment of debts - A banker friend of mine who's task is into generating loans, she confirmed my quick and short response. She also mentioned to me that in their bank, they would usually give a 90 day extension for the debtors to pay off their dues. Penalties are also waived off.

So, if you are affected by Yolanda and your concern is on the payment of your outstanding debts, just approach your creditor and explain to them the situation. I'm pretty sure they will be more lenient with their debtors.

How can they rebuild their lives?

So, yeah! How can one protect one's self from this kind of risk? Time and again, I have heard of studies stating how Japan gets to rebuild itself even it being one country that get's hit by a lot of calamities. The answer to this is INSURANCE.

Japan is the second biggest insurance market in the world after the U.S. and generates nearly 20% of global premiums. In our industry training, it has been shared to us how Japan picks itself up after someone passes away. A Japanese have an average of 7 insurance policies. So, when a Japanese dies, his beneficiaries receives funds that can help them rebuild their lives.

Basically, if we Filipinos learn to understand and harness the magic of insurance, rebuilding would be a little bit more easier.

Pioneer, one of Honeycomb's financial instrument provider, has HomeMaster under it's Non-life insurance arm. I will not be explaining in full detail all the benefits but here are some that could have addressed the situation of those greatly affected by Yolanda and other calamities or "acts of God".

HomeMaster benefits:

HomeMaster benefits:

- Protection against the following perils:

- fire and lightning

- smoke

- vehicle impact

- explosion

- falling aircraft

- burglary or robbery

- bursting and/or overflowing of water tanks and pipes

- earthquakes* (at insured's option)

- typhoon* (at insured's option)

- flood* (at insured's option)

- Coverage for Valuable Items

- Aside from insuring the building, it's improvements, and the standard household contents, you can also secure coverage for declared valuable items such as jewelry, fine art and antiques.

- Protection for Your Living Standards

- When the property you occupy becomes uninhabitable due to damages caused by any of the insured perils, HomeMaster will reimburse you for any necessary increase in your living expenses should you need to move in to a temporary residence. This provides you and your family financial assistance to keep on living comfortably.

- Have the resources to rebuild your home and all its amenities.

- Have the most comprehensive cover for your residence to include perils that may not be covered by standard home insurance.

- Cover for your medical expenses should any of your loved ones get into an accident.

- Provide financial assistance should an accident result in a family member's disablement or death.

- Protect you from any legal liability should you cause bodily injury or property damage to any third party.

- Enjoy savings on your premiums and convenience as you get Personal Accident, Property and Liability insurance in one package.

We can't keep on relying on outside help to rebuild our lives. There are ways to minimize our exposure to the damages of these kind of calamities. Unfortunately, majority of the population have no idea of what's available out there.

As they say, "Nobody plans to fail, they just fail to plan."

So, let's all learn the lesson here. There are ways to manage these risks, it's a matter of asking the right people how. We can help you protect your biggest investment. You may reach us via admin@honeycombfc.com or reach us on Facebook.